A strange thing is happening in the market.

India is still one of the fastest-growing large economies. Its consumer story has not vanished. Its mutual fund investors are still putting money into SIPs. Every week, another founder, minister or analyst talks about artificial intelligence as the next great Indian opportunity.

But foreign investors are walking out.

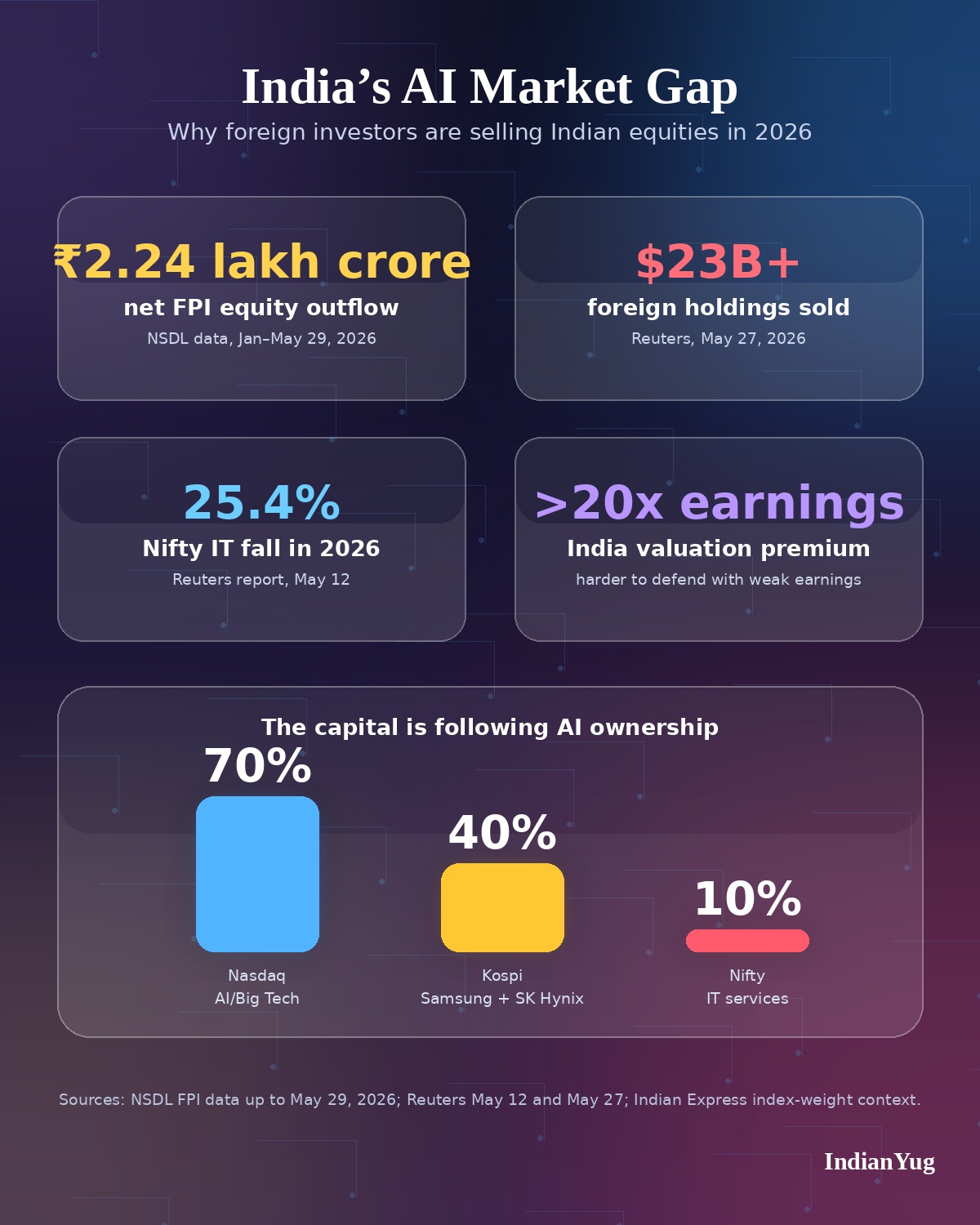

Not slowly. Not symbolically. According to NSDL data up to May 29, 2026, foreign portfolio investors had sold ₹2.24 lakh crore worth of Indian equities this calendar year. Reuters separately reported that overseas investors had sold more than $23 billion of Indian holdings in 2026, already surpassing last year’s record outflows.

That is the surface story.

The deeper story is more uncomfortable: global money is not just leaving India because Indian stocks are expensive. It is leaving because the world’s biggest equity trade is artificial intelligence, and India has very little listed exposure to sell.

India has coders. India has IT services. India has AI ambition.

What it does not yet have is an Indian Nvidia, an Indian TSMC, an Indian SK Hynix, or even a listed AI-native software giant large enough to pull global capital into the country.

The Numbers Behind the Exit

The foreign selling is not a vague mood. It is visible in the official flow data.

NSDL’s calendar-year FPI table shows equity outflows of ₹35,962 crore in January, an inflow of ₹22,615 crore in February, then heavy selling again: ₹1.17 lakh crore in March, ₹60,847 crore in April, and ₹32,963 crore in May up to May 29. The net equity outflow for 2026 stood at ₹2,24,932 crore.

That is roughly ₹2.25 lakh crore of foreign money removed from Indian equities in five months.

Reuters’ May 27 analyst poll put the same pressure into market context. The Nifty 50 was already down about 8.5% in 2026 at the time of the report. A poll of 24 analysts, conducted between May 15 and May 27, forecast the Nifty at 26,000 by the end of 2026. If that happens, Reuters said, the index would post its first annual decline since 2015.

The selling has been softened by domestic money. Indian retail investors and domestic institutions have acted like shock absorbers. Without them, the fall could have been sharper. CNBC-TV18, carrying the Reuters report, quoted Aman Sethia of Groww as saying that domestic institutional and retail liquidity had held the market up; without it, the Nifty may have been closer to 19,000 or 20,000 over the past year.

That support matters. But it also hides the scale of the foreign exit.

Indian households are still buying India. Global investors are asking a harder question: where is India’s AI trade?

Why AI Has Changed the Market Map

For years, India’s market pitch was simple. It had growth, scale, demographics, reform, consumption and a deep IT services sector. That was enough to attract global capital at premium valuations.

Then AI changed what global investors wanted.

The last leg of the global equity rally has not been evenly spread. It has been concentrated in markets that own the hardware, infrastructure and platforms behind artificial intelligence. The United States has Nvidia, Microsoft, Alphabet, Amazon and other large AI-linked companies. Taiwan has TSMC. South Korea has Samsung Electronics and SK Hynix.

India has world-class IT service exporters, but they are not the same thing.

The Indian Express pointed out the index difference clearly. Big tech and AI-linked companies make up about 70% of the Nasdaq. Samsung and SK Hynix account for more than 40% of South Korea’s Kospi. In India, IT services have only about 10% weight in the Nifty, and even those companies are being treated by investors less as AI winners and more as AI-disruption risks.

That distinction is brutal.

In the old outsourcing cycle, India benefited when global companies needed more software work done cheaply and at scale. In the AI cycle, investors are rewarding companies that sell chips, cloud infrastructure, AI platforms, frontier models, data-centre capacity and automation tools.

India is a huge user of these technologies. It is not yet a large listed producer of them.

The Old IT Model Is Under Pressure

The sharpest sign of this anxiety is visible in Indian IT stocks.

Reuters reported on May 12 that India’s IT index had hit its lowest level since May 2023. The Nifty IT index was down 25.4% so far in 2026, making it India’s worst-performing sector, compared with a 9.7% drop in the Nifty 50 at that point.

The worry is not that TCS, Infosys, HCLTech or Wipro will disappear. These are large, capable companies with deep client relationships. The worry is that their old growth engine may not work the same way if AI reduces the need for large teams, long maintenance contracts and billable-hour-heavy software delivery.

Reuters had flagged the pressure earlier too. In February, it reported that Indian software exporters lost $22.5 billion in market value in a week after a global selloff in software stocks linked to AI disruption fears. That report described India’s IT industry as a sector built on labour-intensive outsourcing and facing a possible structural shift.

One estimate cited by Reuters from Motilal Oswal said 9% to 12% of industry revenues could be eliminated over four years. Jefferies warned that application services, which account for a large share of revenue for many firms, could face growth pressure.

There are more optimistic voices as well. Some analysts argue that AI will create new consulting, migration, data and governance work. Indian IT companies themselves are building AI offerings and retraining employees. That may prove true over time.

But markets do not wait for five-year transformation stories when another market already has the chips.

Right now, global capital sees clearer AI earnings in Taiwan, South Korea and the United States than in India.

India’s Valuation Premium Is Harder to Defend

The AI gap would be easier to ignore if Indian stocks were cheap.

They are not.

Reuters noted that Indian equities were trading at more than 20 times earnings, above most major European and emerging markets, while offering one of the world’s lowest dividend yields. That premium was easier to justify when earnings growth looked strong, and India was seen as Asia’s most attractive market.

But when earnings slow and the global growth trade moves elsewhere, the premium becomes a problem.

This is the market’s uncomfortable calculation: why pay a premium for India if the fastest earnings upgrades are in AI hardware and infrastructure outside India?

That question becomes sharper when oil prices and the rupee enter the picture. Reuters’ poll also cited risks from the US-Israel-Iran conflict, higher energy prices and a wider current account deficit. India is a major oil importer. If crude rises, import bills rise. If imports rise faster than exports, pressure builds on the rupee. If the rupee weakens, foreign investors lose money even before stock performance is counted in dollar terms.

So the selloff is not only about AI. It is about AI plus valuations, AI plus weak earnings, AI plus oil vulnerability, AI plus currency risk.

AI is the new lens through which old weaknesses look bigger.

The Irony: India Has AI Talent, But Not AI Ownership

This is the part that should worry policymakers and investors most.

India is not absent from the AI revolution because Indians lack talent. Indians are building models, products, chips, research teams, and AI startups across the world. Indian engineers sit inside the global companies that are leading the boom.

The problem is ownership.

A lot of Indian AI talent creates value inside foreign companies. A lot of Indian AI consumption creates revenue for foreign platforms. A lot of Indian enterprise AI adoption may improve productivity, but it does not automatically create a large listed Indian AI champion.

That is why the stock market reaction looks so harsh.

A country can have talent and still miss the equity trade. It can have users and still miss the profit pool. It can have service providers and still fail to own the infrastructure layer.

This is what global investors are pricing.

They are not saying India has no AI future. They are saying India does not yet offer enough ways to buy that future in public markets.

What Could Change the Story

The story is not fixed. India can still build serious AI-linked listed value, but it needs more than speeches and pilot projects.

First, India needs hardware and infrastructure depth. Data centres, power availability, cooling systems, cloud infrastructure, networking, semiconductor design, packaging and electronics manufacturing are no longer side sectors. They are the industrial base of AI.

Second, India needs AI-native companies that create their own margins, not only service companies that implement someone else’s tools. Global investors reward ownership of intellectual property, platforms and infrastructure more than headcount scale.

Third, Indian IT companies need to prove that AI can expand their revenue, not only compress their billing. That means showing measurable AI-led deals, higher productivity, better margins and products that clients cannot easily replace with in-house tools.

Fourth, public-market investors need visibility. If India’s AI companies remain private, small or buried inside conglomerates, foreign funds will continue to look elsewhere for clean AI exposure.

Finally, earnings must catch up with valuations. Domestic flows can support the market for a long time, but they cannot permanently replace foreign confidence if corporate earnings disappoint.

The Real Warning

The foreign investor exit is not a rejection of India’s long-term economy. It is a warning about India’s place in the next profit cycle.

For two decades, India benefited from being the world’s back office. That model created wealth, jobs, campuses, dollar revenues and a powerful services industry. But AI is changing the hierarchy. The market is now rewarding those who own compute, chips, models, cloud platforms and automation layers.

India is still strong in people.

The AI boom is rewarding ownership.

That is the gap foreign investors are seeing. Until India closes it, domestic investors may keep buying the India story, but global capital will keep asking the same question before it returns: where is the Indian company that truly owns the AI boom?