The Great Indian Startup Illusion: Built on Cheap Labour, Funded by Hype

Ghaziabad/Noida: At 2 AM on a rain-soaked Noida street, a 22-year-old delivery rider checks his phone. His app shows he has earned ₹187 across nine hours of work today — before platform fees, insurance deductions, and the daily scooter-fleet rental. He has not eaten since noon. The app’s algorithm, designed by one of India’s most valuable startups, offers him a ₹5 bonus if he completes two more deliveries before 3 AM. He takes the order. He has no choice.

This rider is not an anomaly. He is the foundation upon which a $100-billion startup economy is being built. And the uncomfortable truth that India’s venture capital ecosystem does not want to talk about is this: most of what passes for innovation in this country is not innovation at all. It is a copy-paste business model dressed in venture capital, sustained by labour that costs almost nothing, protected by the absence of regulation, and rewarded with valuations that have nothing to do with technological breakthroughs.

Over the last decade, India has produced more unicorns than almost any country outside the United States and China. But ask yourself this: how many of them have built something the world has never seen before? How many hold patents that matter? How many invest even one percent of their valuation into research and development?

The answer is uncomfortable.

Copy, Don’t Create: The Silicon Valley Reheating Machine

India’s startup playbook is painfully predictable. Step one: identify a business model that has already proven itself in the United States or China. Step two: build a basic app that replicates the core functionality. Step three: raise a seed round on the strength of a “Tinder for X” or “Uber for Y” pitch deck. Step four: call it innovation and wait for the valuation to follow.

Food delivery startups cloned DoorDash and Grubhub. Ride-hailing apps copied Uber and Lyft. Quick commerce brands replicated GoPuff and Instacart. Social commerce platforms mirrored Pinduoduo. Fintech apps took everything from PayPal to Klarna and rebranded it for Indian users. Edtech companies copied Coursera, then added aggressive sales calls.

None of this required fundamental research. None of it involved building original technology. The heavy lifting — the algorithms, the architecture, the business logic — had already been done by someone else. The Indian version simply needed a cheaper workforce to execute it.

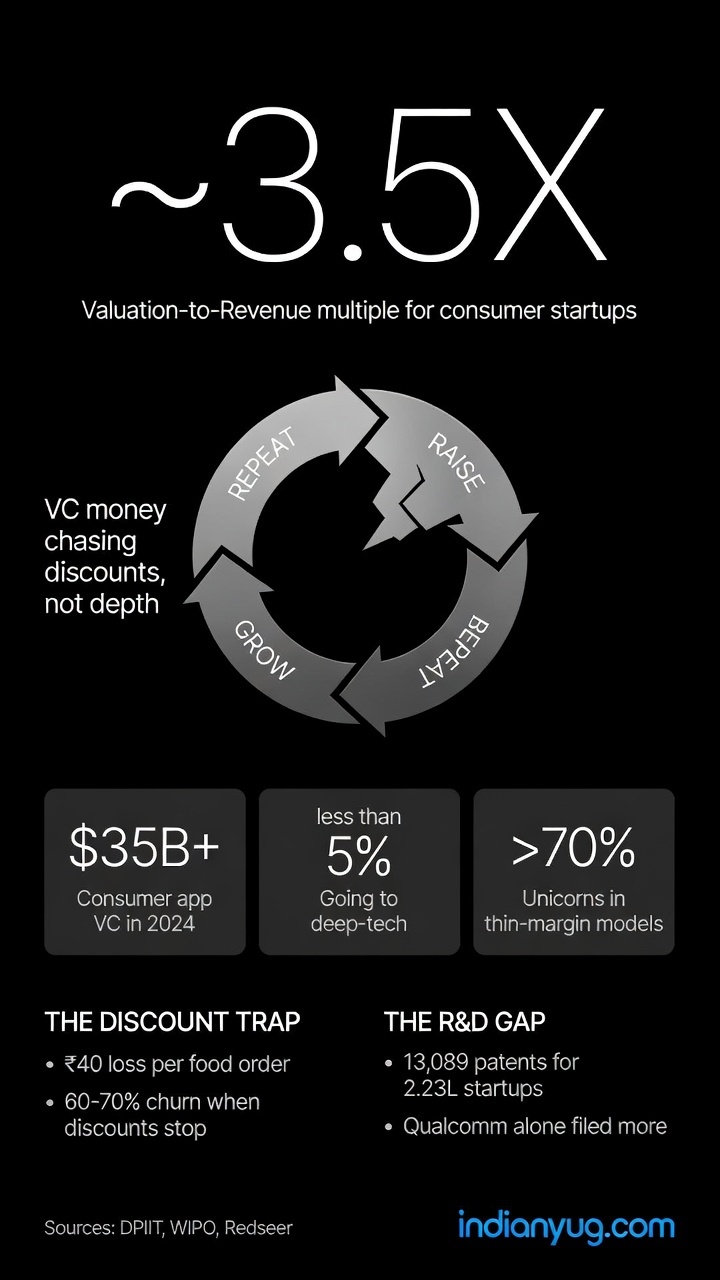

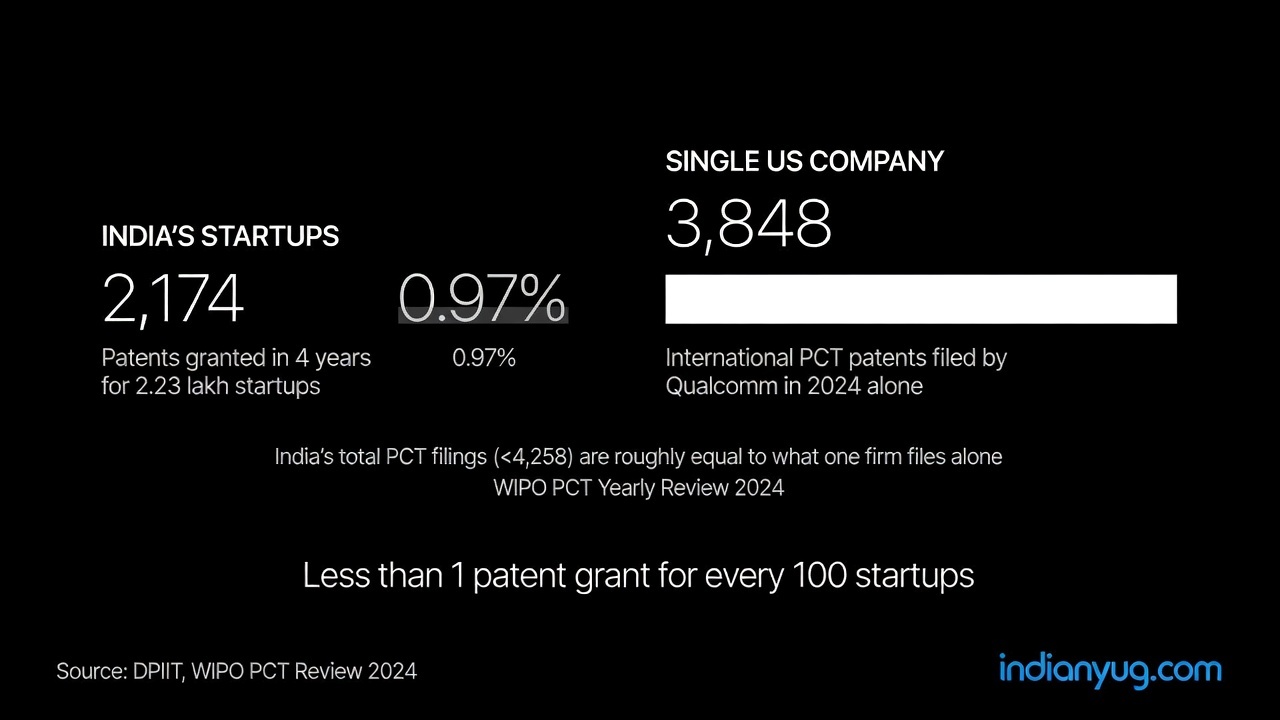

This is not an accusation. It is a description of a system that rewards speed over depth. As of March 2026, India had over 2.23 lakh DPIIT-recognized startups. Between FY21 and FY25, startups filed 13,089 patent applications — of which only 2,174 were granted. With notable exceptions, the overwhelming majority of consumer-facing startups have not filed a single meaningful international patent. And when it comes to R&D spending as a percentage of revenue, most consumer-facing Indian startups lag far behind their global peers.

The Indian startup story is not a story of invention. It is a story of adaptation — and adaptation, when the only variable being changed is the cost of labour, is not innovation.

Growth Over Technology: Valuations Before Breakthroughs

Here is a simple test of where a startup’s priorities lie. Look at how it spends money.

A genuinely innovative company — think ASML in the Netherlands, TSMC in Taiwan, or even a modest biotech firm — spends heavily on R&D. Research is the engine. Patents are the output. Technology is the product.

Now look at India’s celebrated unicorns. For most consumer-facing unicorns, the largest expense lines in their balance sheets are not laboratories or engineering teams. They are marketing budgets, sales commissions, and discount subsidies. Customer acquisition cost is the metric that matters. Monthly active users drive valuation. Gross merchandise value is the number that impresses investors.

Patents? A rounding error.

Here is a data point worth sitting with. In 2023, Qualcomm — a single American semiconductor firm — filed 3,848 international patent applications under WIPO’s Patent Cooperation Treaty (PCT). India’s total PCT filings across every startup, university, and research institution combined? Fewer than 4,258 — the cutoff for the global top 10. In other words, one US company filed more international patents than the entire Indian startup ecosystem. Reliance Jio, often cited as India’s great tech success, is fundamentally a pricing revolution, not a technology revolution. The underlying network infrastructure was supplied by Samsung and Nokia. The phones were manufactured by Chinese OEMs. The innovation was not in the technology — it was in the pricing model.

This pattern repeats across the ecosystem. The founder who can show hockey-stick user growth will raise capital faster than the founder who can demonstrate a genuine scientific breakthrough. The marketplace that can offer the deepest discounts will attract the most users. And the app that can squeeze the most deliveries out of a single rider in a single night will have the best unit economics.

The system does not reward building better technology. It rewards growing faster than the competition — and the fastest way to grow is to spend more on discounts and marketing, not on R&D.

Cheap Labour Is the Real Moat

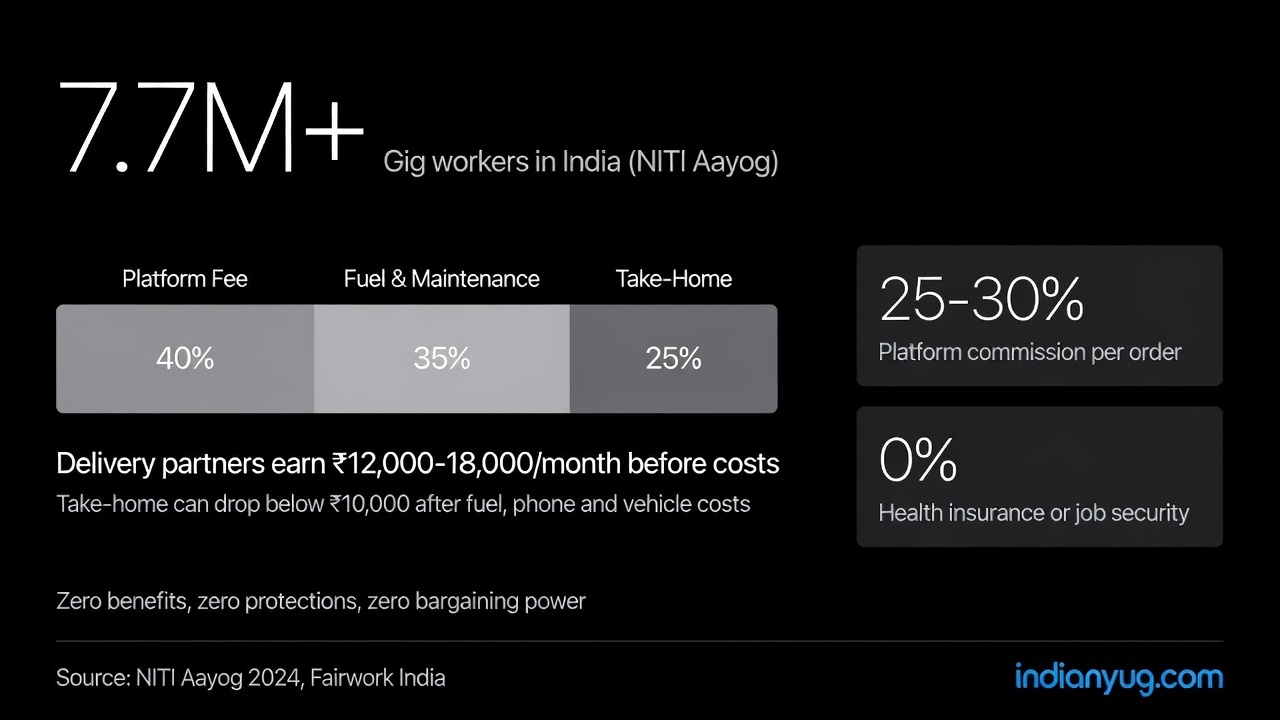

Every investor presentation from a gig-economy startup includes a slide about “supply-side aggregation.” What this phrase really means is: a large pool of desperate workers who have no alternative.

India has one of the largest informal workforces in the world. Over 90 percent of the country’s labour force works in the unorganised sector. This is the pool that gig platforms draw from. A delivery rider in Gurugram, a cab driver in Bengaluru, a domestic worker in Mumbai, a field technician in Lucknow — they come from villages and small towns where there are no jobs, no safety nets, and no prospects.

The startup does not create their job. It intermediaries their desperation.

Here are the numbers that no funding round press release will share with you. A Fairwork India report from 2023 rated India’s major gig platforms on working conditions. The average score across 12 platforms was 4 out of a possible 10. None scored above 7. The lowest — a major food delivery platform — scored 2. Key findings included unpredictable earnings, sudden algorithm changes that reduced pay, lack of written contracts in local languages, and zero collective bargaining rights.

A delivery rider in Delhi earns, on average, between ₹12,000 and ₹18,000 per month before expenses. After fuel, phone data, and vehicle rental — because most riders do not own the scooters they ride — the take-home pay drops below ₹10,000. For this, they work 12 to 14-hour shifts, six days a week, with no overtime pay, no health insurance, no paid leave, and no job security.

If they complain, the algorithm deactivates them. No hearing. No appeal. Just a notification on the app.

This is not an unfortunate side effect. This is the business model. The entire valuation of these companies rests on the assumption that labour costs will remain low. The moment Indian gig workers demand minimum wage, social security, or collective bargaining rights, the math behind every unicorn collapses.

Discounts Funded by Investors: The Ponzi Pattern

How does a startup go from zero to a billion-dollar valuation in three years? The answer is subsidies that no rational business would offer on its own.

A plate of biryani delivered to your home for ₹49. A cab ride across Delhi for ₹99. A grocery delivery in ten minutes with no minimum order. These prices do not reflect the real cost of delivery. They reflect the willingness of venture capital investors to burn cash in exchange for user acquisition.

Here is how the cycle works. A startup raises $100 million from a venture capital fund. It spends $80 million on discounts and marketing to acquire users. It reports hypergrowth in monthly active users. It raises another round at a higher valuation. The investors from the first round get to mark up their investment on paper. Early employees get to exercise their stock options. The founder becomes a paper billionaire. The media writes glowing profiles.

Then the subsidies stop.

Once the startup has cornered the market, the discounts disappear. Prices rise. Delivery fees increase. Surge pricing kicks in. The customer who was paying ₹49 for biryani is now paying ₹149 plus a platform fee plus a delivery charge plus a surge multiplier.

The worker, meanwhile, is earning less than before, because the platform must now show profitability to its public market investors. The easiest cost to cut is the one that walks, talks, and has no union.

The tragic irony is that the pattern is now so well-documented that it is almost academic. Amazon did it. Uber did it. Didi did it. Nearly every marketplace built on the subsidised-growth model eventually raises prices while squeezing suppliers. Yet Indian investors continue to fund the same playbook with no evidence that the outcome will be different this time.

The Innovation Gap: What India Is Not Building

Stand at a startup conference in Bengaluru and look at the booths. You will see food delivery, grocery delivery, medicine delivery, pet food delivery, furniture delivery, alcohol delivery, and document delivery. You will see ride-hailing and bike-sharing and scooter-rental and bus-booking. You will see a hundred variations of the same marketplace model, each one promising to deliver something marginally different in a marginally shorter time.

Now walk to the other end of the convention hall, where the genuinely deep-tech startups are supposed to be. The section is usually half-empty.

Where are the Indian startups building:

AI foundational models — not wrappers over ChatGPT, but original architectures trained on Indian languages and Indian data?

Semiconductor fabrication — not chip design services for foreign clients, but actual fabs making Indian-designed processors?

Robotics — not delivery bots that follow sidewalk lines, but industrial automation that could revive Indian manufacturing?

Medical technology — not telemedicine apps, but diagnostic devices and drug discovery platforms that could reduce India’s healthcare costs?

Clean energy — not solar panel installation marketplaces, but next-generation battery storage, green hydrogen, or carbon capture?

Space technology — beyond the satellite-launch services that ISRO already commercialised, to deep-space propulsion, asteroid mining, or space-based manufacturing?

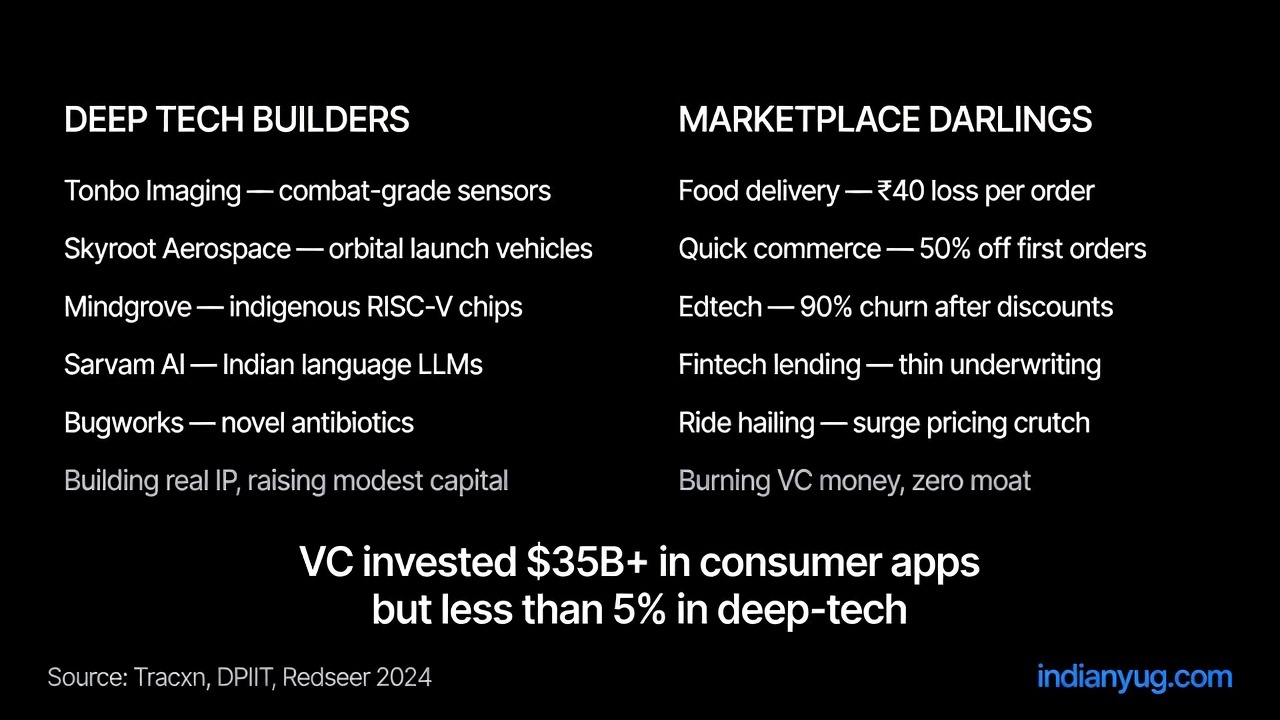

To be fair, this picture is not completely blank. India has genuine bright spots. Defence startups like Tonbo Imaging (night-vision sensors) and Big Bang Boom Solutions are building proprietary hardware for the armed forces. Space-tech ventures like Skyroot Aerospace and Agnikul Cosmos have developed indigenous launch vehicles. Semiconductor designers like Mindgrove Technologies and Oravel Semiconductor are creating original chip architectures. Biotech firms like Bugworks Research are developing novel antibiotic classes. And in AI, startups like Sarvam AI are building foundational language models for Indian languages rather than wrapping foreign APIs. These are exceptions, not the norm — and they prove the point. Where deep-tech startups do exist, they struggle for capital, face longer gestation periods, and rarely receive the media attention that a new food delivery unicorn commands.

Consider the contrast with China. Meituan — a food delivery and lifestyle company, the very category India claims cannot support deep tech — recently open-sourced LongCat-2.0, a large language model with 1.6 trillion parameters and a million-token context window. What makes it remarkable is not just its scale but the fact that it was trained entirely on domestic Chinese semiconductors, bypassing the Nvidia chips that power most of the world’s AI models. A food delivery company in Beijing is building foundational AI on homegrown hardware. Indian food delivery companies are still fighting over which one can deliver a ₹49 biryani faster.

An AI chip startup might take eight years and $200 million to produce a meaningful result. A food delivery app can show 200 percent user growth in eight months on $20 million of discounts. The choice for investors is obvious. And that is precisely the problem.

The Valuation Game: Rounds Over Results

Success in India’s startup ecosystem is measured by one thing: how much money you have raised, not what you have built.

A startup’s funding history is treated as its primary credential. Headlines announce the Series A, Series B, Series C as if each round is itself an achievement. LinkedIn bios proudly declare “raised $50 million from Sequoia and Accel.” The implication is that the ability to convince investors to write a cheque is synonymous with building a valuable company.

It is not.

In 2021, at the peak of the funding boom, Indian startups raised over $42 billion. In 2023, as global capital tightened, many of the same startups were raising down rounds, laying off staff, or shutting down entirely. Companies that had been valued at over a billion dollars were found to be worth a fraction of that when subjected to the scrutiny of a down round.

The reason is simple: valuations in the Indian startup ecosystem are often less a reflection of business fundamentals than they are of narrative momentum. A startup can lose money on every transaction, have no proprietary technology, and treat its workers poorly — and still command a billion-dollar valuation, as long as it can tell a compelling story about total addressable market, growth trajectory, and founder-market fit.

This is not an indictment of any single company. It is a structural flaw in how capital allocates itself in the Indian innovation economy. When the metric of success is the ability to raise the next round, the incentive is to optimise for the next round — not for the long-term health of the business, the welfare of the workforce, or the technological advancement of the country.

Convenience at a Hidden Cost

Let us be honest about our own role in this system.

The consumer who orders biryani at ₹49 is not thinking about the rider who delivers it. The customer who books a cab at ₹99 does not wonder whether the driver can afford to maintain the car. The urban professional who gets groceries delivered in ten minutes does not consider the warehouse worker speed-packing at a rate that would be illegal in most developed economies.

Convenience is a powerful drug. And in India, it is being sold at a price that is not reflected in the transaction.

Every time a platform offers a service below cost, the difference is paid by someone. If not the investor’s capital today, then the worker’s income tomorrow. The idea that venture capital subsidies create permanent value is a myth. They create temporary market distortions that benefit urban consumers at the expense of vulnerable workers — all while generating the illusion of a thriving technology sector.

The gig worker is the invisible balance sheet. When the platform reports improving unit economics, it is often because the algorithm has figured out a new way to pay the worker less. When the company declares it has achieved “path to profitability,” it frequently means it has squeezed just enough out of the delivery fleet to cover the difference.

This is not efficiency. It is cost transfer.

The Wrong Incentives: Why Capital Fails Deep Tech

The problem is not that Indian entrepreneurs are lazy or unintelligent. The problem is that the incentive structure of Indian venture capital actively discourages deep technological work.

Consider the typical journey of a deep-tech founder in India. She needs patient capital — investment that does not expect an exit within five to seven years. She needs regulatory support — clear policies on intellectual property, data sovereignty, and technology transfer. She needs infrastructure — reliable power, high-bandwidth connectivity, access to advanced manufacturing facilities. And she needs a talent pipeline that values depth of expertise over breadth of startup experience.

What she gets is none of these.

Indian venture capital funds typically have a seven-to-ten year fund life, which means they need exits within that window. Deep tech often takes longer. The result is that even the most well-intentioned deep-tech fund is under pressure to invest in companies that can show rapid commercial traction — which brings them back to consumer apps.

The government’s initiatives — Startup India, the National Deep Tech Startup Policy, the Anusandhan National Research Foundation — are steps in the right direction. But their impact remains marginal compared to the sheer volume of private capital flowing into copycat consumer apps. In 2023, deep-tech startups received less than 5 percent of total venture capital funding in India.

The Counterargument: Market Demand Creates Market Solutions

There is a case to be made on the other side. It goes like this.

India is a price-sensitive market. Consumers in this country will not pay a premium for innovation. They will pay the lowest possible price for adequate service. The startup model that works in India is the one that delivers acceptable quality at the lowest cost. That is what the market rewards.

Furthermore, the gig economy has created millions of jobs in a country that desperately needs them. For a young person from a village in Bihar or Uttar Pradesh, a delivery job — even a poorly paid one — may still be better than anything available in their hometown. The platform may not pay well by urban standards, but it pays more than agricultural wage labour or daily-wage construction work.

And there is this: marketplaces are not inherently bad. They connect supply with demand efficiently. The delivery app that brings food to an elderly person’s home, the cab that lets a woman travel safely at night, the quick commerce that saves time for a working parent — these are real benefits that consumers value.

The counterargument is not wrong. It is simply incomplete. Yes, market demand favours low prices. Yes, gig jobs are better than no jobs. Yes, marketplace efficiency has real benefits. None of these truths invalidate the observation that the system is rigged against workers and against genuine innovation. A country of 1.4 billion people can do better than the choice between desperate gig work and nothing at all.

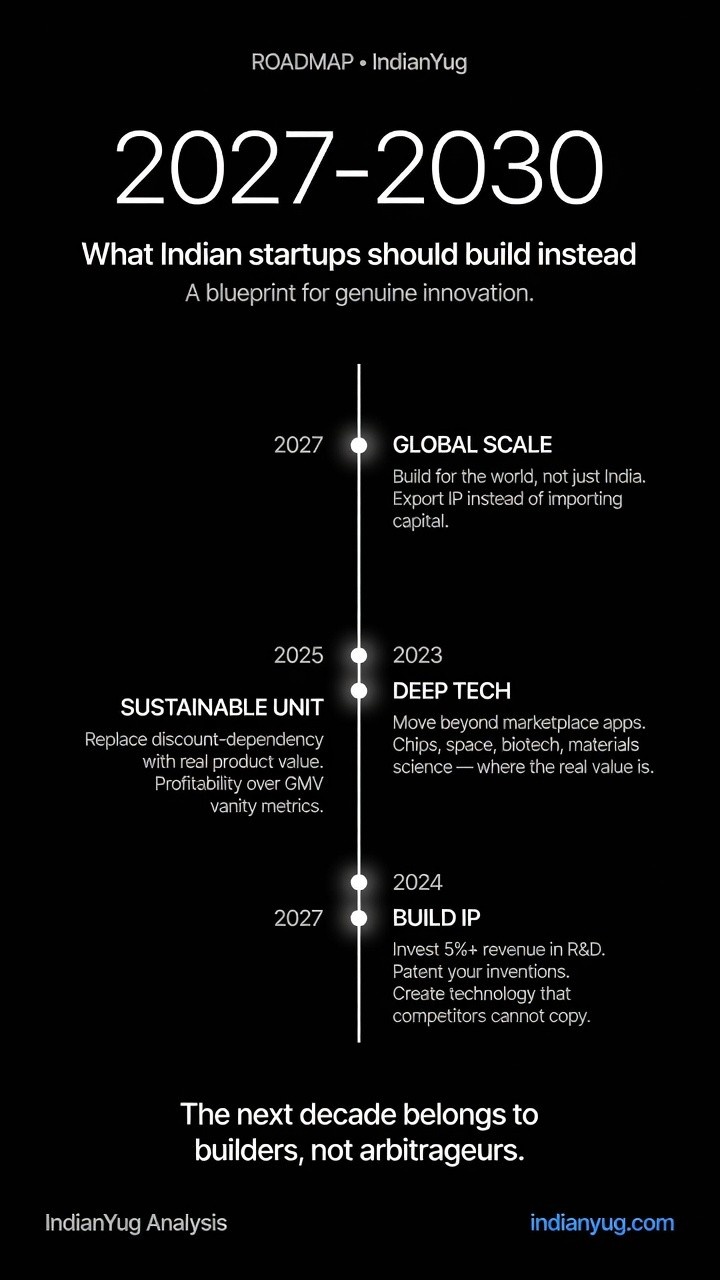

Reckoning: Where Does India Go From Here?

This is not a call to dismantle the startup ecosystem. It is a call to grow up.

India’s technology sector is approaching an inflection point. The easy growth — the copy-paste model, the discount-fueled user acquisition, the venture-capital subsidy — is running out of steam. Global capital is no longer flowing freely. Public markets are scrutinising unit economics. Workers are beginning to organise. Regulators are starting to pay attention.

What comes next will determine whether India builds a genuine innovation economy or remains a market for other people’s technology, staffed by people who cannot afford to live in the cities they service.

The path forward requires three things.

First, a shift in how capital is allocated. India needs patient, risk-tolerant funding for deep-tech ventures — not just more consumer-app SPVs. The government’s deep-tech fund is a start, but it must be scaled by an order of magnitude.

Second, labour protections that acknowledge the gig economy. A minimum earnings floor, portable benefits, transparent algorithm governance, and the right to collective bargaining are not anti-business demands. They are the baseline conditions of a modern economy. Countries in Europe and parts of Southeast Asia have already legislated in this direction. India is falling behind.

Third, a change in how we measure success. Not every startup needs to be a unicorn. Not every founder needs a billion-dollar valuation. The question we should be asking is not how much money a startup raised, but what it built, how it treats its people, and whether it made something that did not exist before.

Sources and References

1. DPIIT Startup India Portal — Over 2.23 lakh recognized startups as of March 2026

2. Economic Survey 2023-24 — Startup patent filings: 13,089 applications (FY21-FY25), 2,174 granted

3. WIPO Patent Cooperation Treaty Yearly Review 2024 — Qualcomm: 3,848 PCT filings (2024); Top 10 PCT origins: 4,258 cutoff

4. Fairwork India Ratings 2023 — Labour conditions on 12 major gig platforms (average score: 4/10)

5. NITI Aayog — India’s Booming Gig and Platform Economy (2022)

6. RBI Bulletin — Analysis of startup funding trends and valuation patterns

7. Meituan / CTOL Digital — LongCat-2.0 LLM: 1.6 trillion parameters, trained on domestic semiconductors

8. Centre for Internet and Society — Platform labour research in India

9. Various company filings with the Registrar of Companies (ROC) for expense breakdowns

The Question That Lingers

If India’s brightest minds are spending their time making deliveries ten minutes faster instead of solving humanity’s hardest problems, are we building a startup ecosystem or just a better marketplace?

The answer to that question will decide what kind of country India becomes in the next twenty years.